Chapter 9 - Tabular Modelling Deep Dive

Just notes for archiving

- Tabular Modeling Deep Dive

They are beautiful. (from my sister's place)

Tabular modeling takes data in the form of a table (like a spreadsheet or CSV). The objective is to predict the value in one column based on the values in the other columns. In this chapter we will not only look at deep learning but also more general machine learning techniques like random forests, as they can give better results depending on your problem.

We will look at how we should preprocess and clean the data as well as how to interpret the result of our models after training, but first, we will see how we can feed columns that contain categories into a model that expects numbers by using embeddings.

In tabular data some columns may contain numerical data, like "age," while others contain string values, like "sex." The numerical data can be directly fed to the model (with some optional preprocessing), but the other columns need to be converted to numbers. Since the values in those correspond to different categories, we often call this type of variables categorical variables. The first type are called continuous variables.

jargon:Continuous and Categorical Variables: Continuous variables are numerical data, such as "age," that can be directly fed to the model, since you can add and multiply them directly. Categorical variables contain a number of discrete levels, such as "movie ID," for which addition and multiplication don't have meaning (even if they're stored as numbers).

At the end of 2015, the Rossmann sales competition ran on Kaggle. Competitors were given a wide range of information about various stores in Germany, and were tasked with trying to predict sales on a number of days. The goal was to help the company to manage stock properly and be able to satisfy demand without holding unnecessary inventory. The official training set provided a lot of information about the stores. It was also permitted for competitors to use additional data, as long as that data was made public and available to all participants.

One of the gold medalists used deep learning, in one of the earliest known examples of a state-of-the-art deep learning tabular model. Their method involved far less feature engineering, based on domain knowledge, than those of the other gold medalists. The paper, "Entity Embeddings of Categorical Variables" describes their approach. In an online-only chapter on the book's website we show how to replicate it from scratch and attain the same accuracy shown in the paper. In the abstract of the paper the authors (Cheng Guo and Felix Berkhahn) say:

:Entity embedding not only reduces memory usage and speeds up neural networks compared with one-hot encoding, but more importantly by mapping similar values close to each other in the embedding space it reveals the intrinsic properties of the categorical variables... [It] is especially useful for datasets with lots of high cardinality features, where other methods tend to overfit... As entity embedding defines a distance measure for categorical variables it can be used for visualizing categorical data and for data clustering.

We have already noticed all of these points when we built our collaborative filtering model. We can clearly see that these insights go far beyond just collaborative filtering, however.

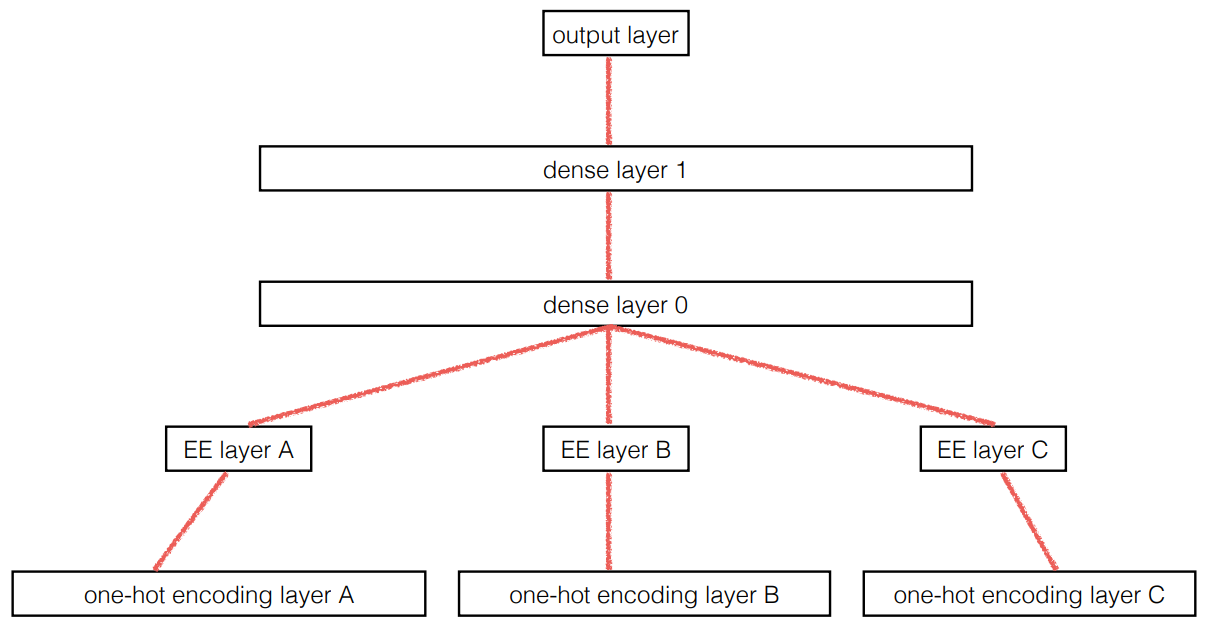

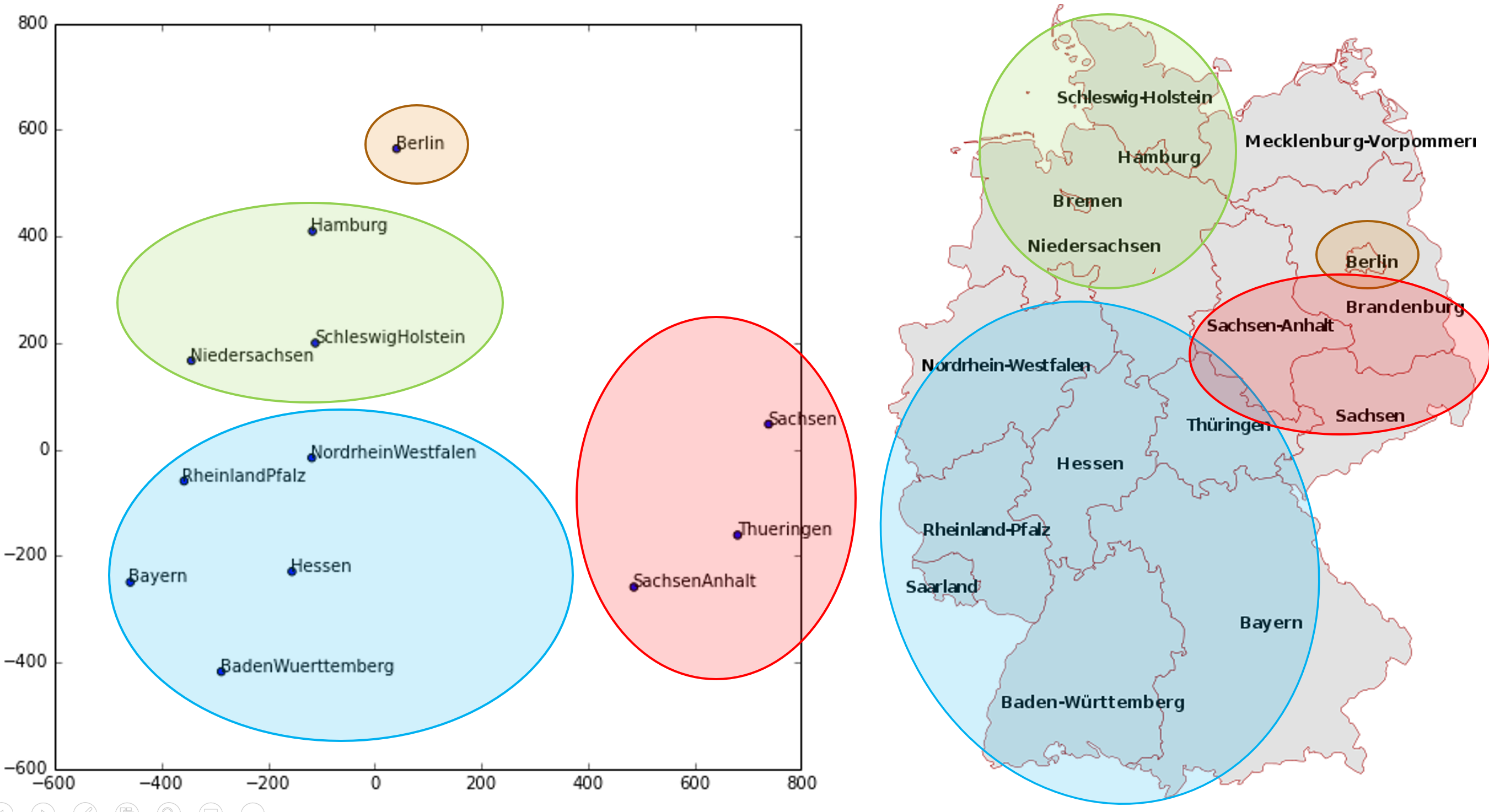

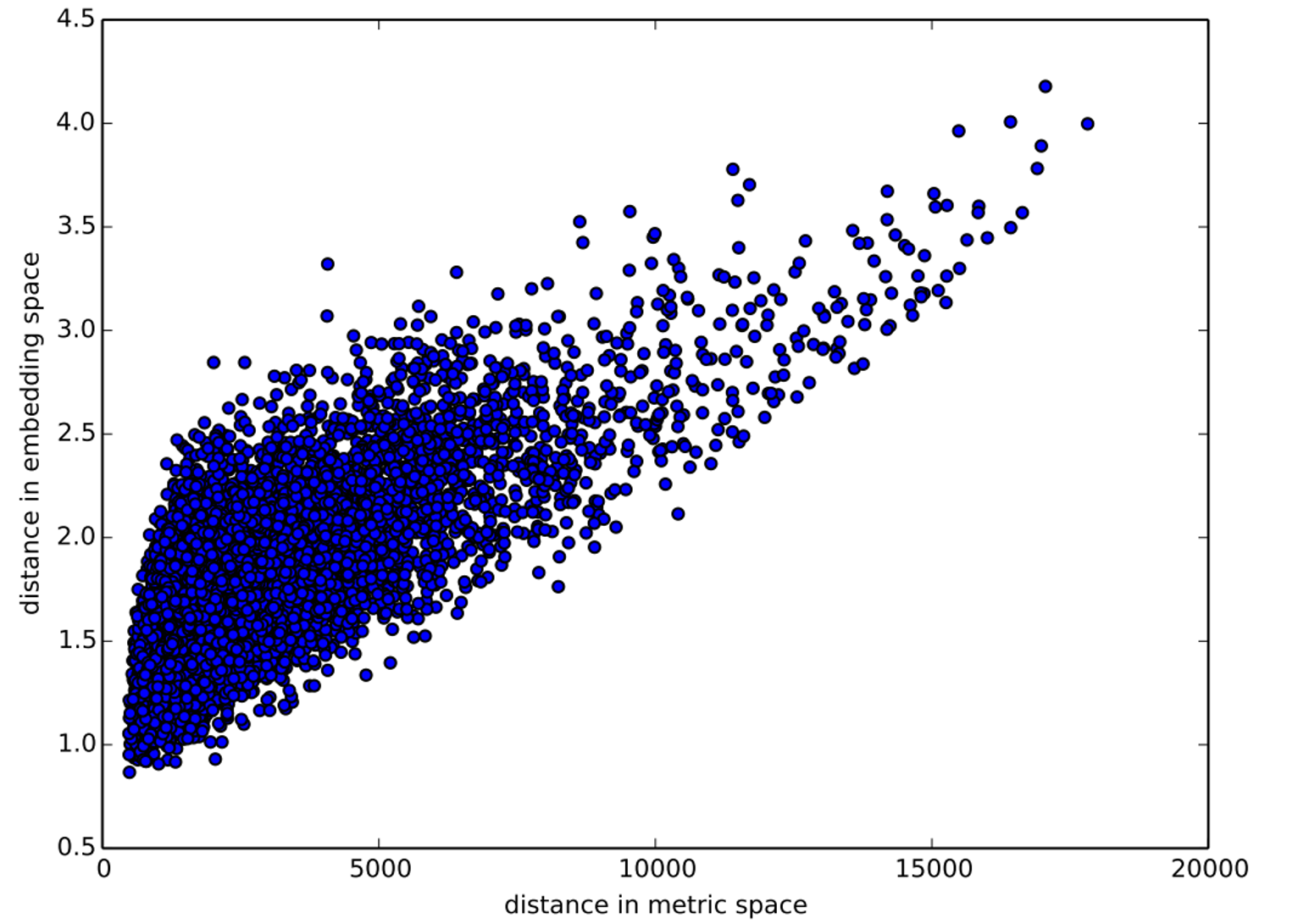

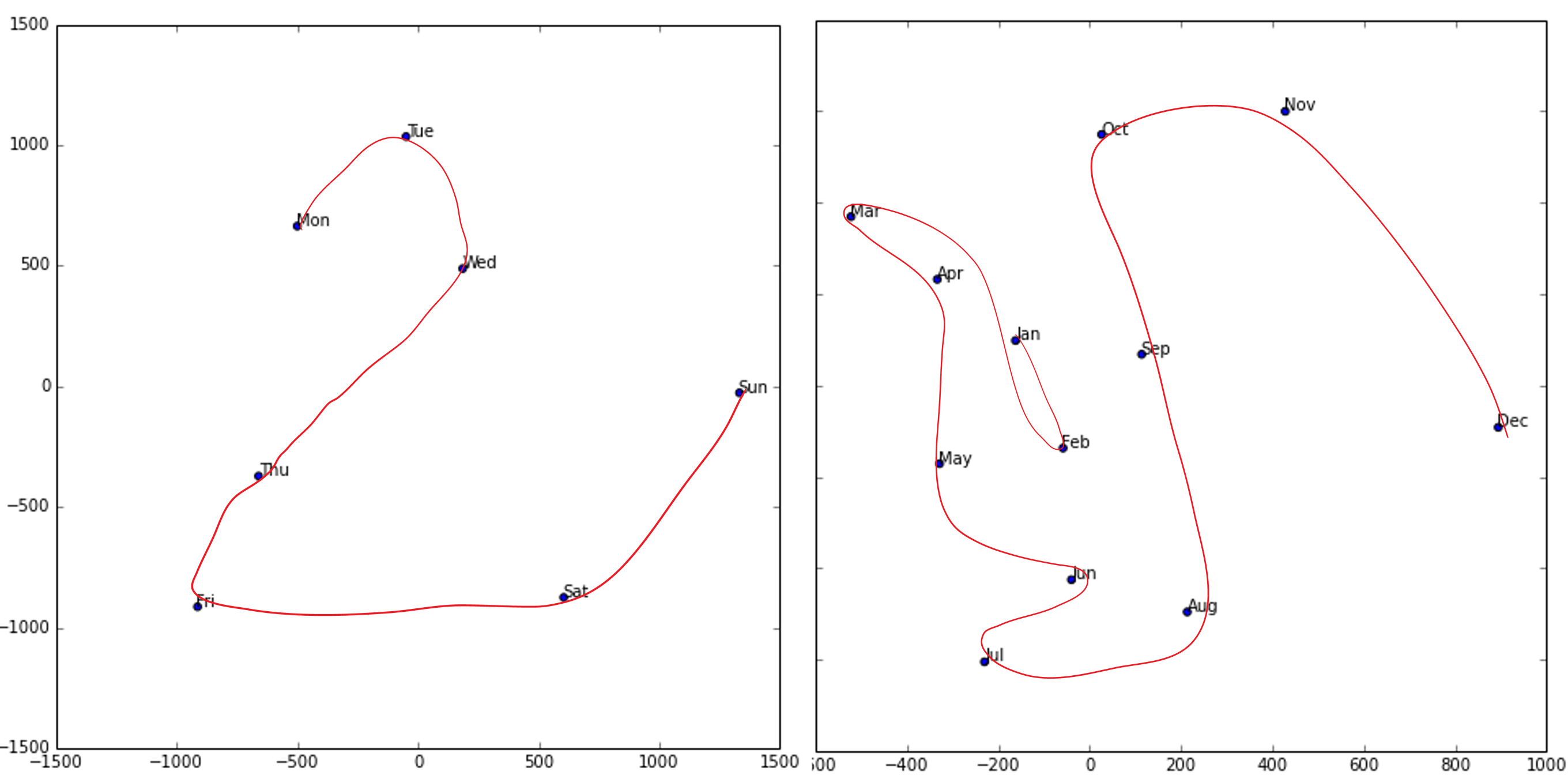

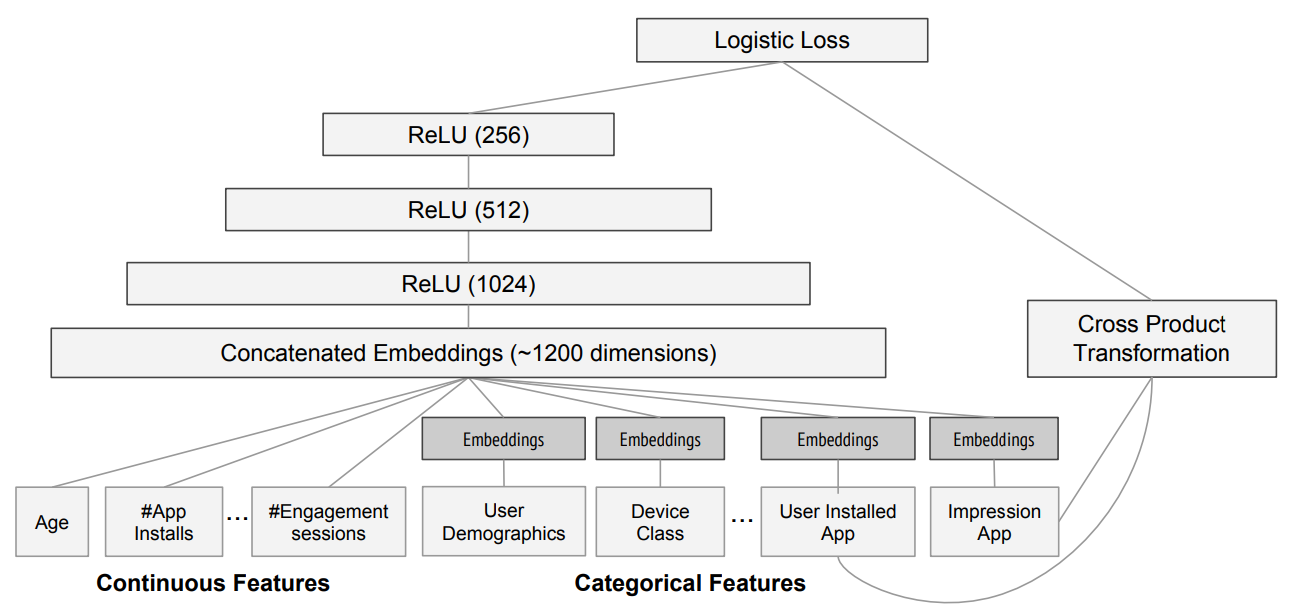

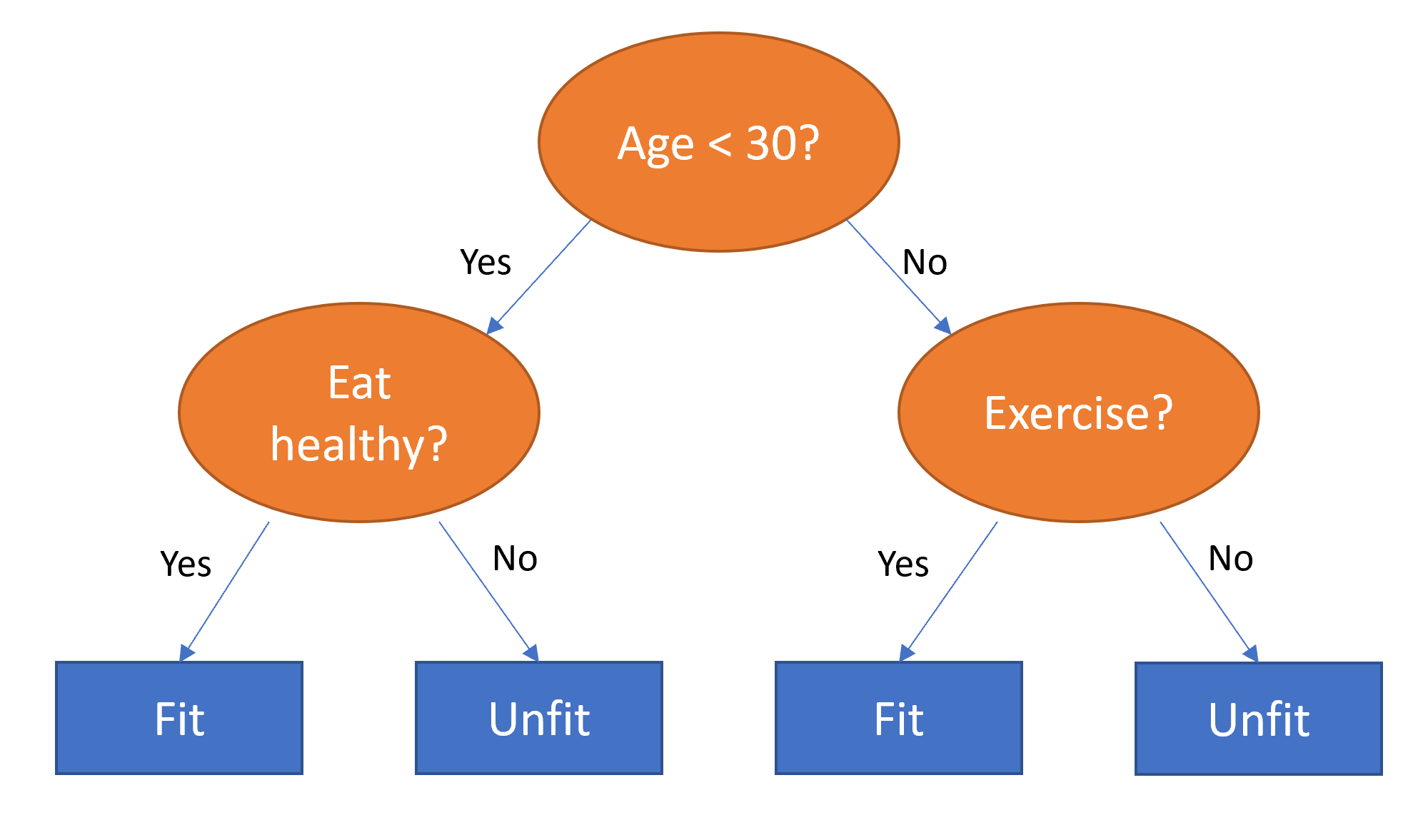

The paper also points out that (as we discussed in the last chapter) an embedding layer is exactly equivalent to placing an ordinary linear layer after every one-hot-encoded input layer. The authors used the diagram in < The insight is important because we already know how to train linear layers, so this shows that from the point of view of the architecture and our training algorithm the embedding layer is just another layer. We also saw this in practice in the last chapter, when we built a collaborative filtering neural network that looks exactly like this diagram. Where we analyzed the embedding weights for movie reviews, the authors of the entity embeddings paper analyzed the embedding weights for their sales prediction model. What they found was quite amazing, and illustrates their second key insight. This is that the embedding transforms the categorical variables into inputs that are both continuous and meaningful. The images in < On the left is a plot of the embedding matrix for the possible values of the Do you remember how we talked about distance between embeddings? The authors of the paper plotted the distance between store embeddings against the actual geographic distance between the stores (see < We've even tried plotting the embeddings for days of the week and months of the year, and found that days and months that are near each other on the calendar ended up close as embeddings too, as shown in < What stands out in these two examples is that we provide the model fundamentally categorical data about discrete entities (e.g., German states or days of the week), and then the model learns an embedding for these entities that defines a continuous notion of distance between them. Because the embedding distance was learned based on real patterns in the data, that distance tends to match up with our intuitions. In addition, it is valuable in its own right that embeddings are continuous, because models are better at understanding continuous variables. This is unsurprising considering models are built of many continuous parameter weights and continuous activation values, which are updated via gradient descent (a learning algorithm for finding the minimums of continuous functions). Another benefit is that we can combine our continuous embedding values with truly continuous input data in a straightforward manner: we just concatenate the variables, and feed the concatenation into our first dense layer. In other words, the raw categorical data is transformed by an embedding layer before it interacts with the raw continuous input data. This is how fastai and Guo and Berkhahn handle tabular models containing continuous and categorical variables. An example using this concatenation approach is how Google does its recommendations on Google Play, as explained in the paper "Wide & Deep Learning for Recommender Systems". < Interestingly, the Google team actually combined both approaches we saw in the previous chapter: the dot product (which they call cross product) and neural network approaches. Let's pause for a moment. So far, the solution to all of our modeling problems has been: train a deep learning model. And indeed, that is a pretty good rule of thumb for complex unstructured data like images, sounds, natural language text, and so forth. Deep learning also works very well for collaborative filtering. But it is not always the best starting point for analyzing tabular data. Most machine learning courses will throw dozens of different algorithms at you, with a brief technical description of the math behind them and maybe a toy example. You're left confused by the enormous range of techniques shown and have little practical understanding of how to apply them. The good news is that modern machine learning can be distilled down to a couple of key techniques that are widely applicable. Recent studies have shown that the vast majority of datasets can be best modeled with just two methods: Although deep learning is nearly always clearly superior for unstructured data, these two approaches tend to give quite similar results for many kinds of structured data. But ensembles of decision trees tend to train faster, are often easier to interpret, do not require special GPU hardware for inference at scale, and often require less hyperparameter tuning. They have also been popular for quite a lot longer than deep learning, so there is a more mature ecosystem of tooling and documentation around them. Most importantly, the critical step of interpreting a model of tabular data is significantly easier for decision tree ensembles. There are tools and methods for answering the pertinent questions, like: Which columns in the dataset were the most important for your predictions? How are they related to the dependent variable? How do they interact with each other? And which particular features were most important for some particular observation? Therefore, ensembles of decision trees are our first approach for analyzing a new tabular dataset. The exception to this guideline is when the dataset meets one of these conditions: In practice, when we deal with datasets that meet these exceptional conditions, we always try both decision tree ensembles and deep learning to see which works best. It is likely that deep learning will be a useful approach in our example of collaborative filtering, as we have at least two high-cardinality categorical variables: the users and the movies. But in practice things tend to be less cut-and-dried, and there will often be a mixture of high- and low-cardinality categorical variables and continuous variables. Either way, it's clear that we are going to need to add decision tree ensembles to our modeling toolbox! Up to now we've used PyTorch and fastai for pretty much all of our heavy lifting. But these libraries are mainly designed for algorithms that do lots of matrix multiplication and derivatives (that is, stuff like deep learning!). Decision trees don't depend on these operations at all, so PyTorch isn't much use. Instead, we will be largely relying on a library called scikit-learn (also known as We don't have time to do a deep dive into all these libraries in this book, so we'll just be touching on some of the main parts of each. For a far more in depth discussion, we strongly suggest Wes McKinney's Python for Data Analysis (O'Reilly). Wes is the creator of Pandas, so you can be sure that the information is accurate! First, let's gather the data we will use. The dataset we use in this chapter is from the Blue Book for Bulldozers Kaggle competition, which has the following description: "The goal of the contest is to predict the sale price of a particular piece of heavy equipment at auction based on its usage, equipment type, and configuration. The data is sourced from auction result postings and includes information on usage and equipment configurations." This is a very common type of dataset and prediction problem, similar to what you may see in your project or workplace. The dataset is available for download on Kaggle, a website that hosts data science competitions. Kaggle is an awesome resource for aspiring data scientists or anyone looking to improve their machine learning skills. There is nothing like getting hands-on practice and receiving real-time feedback to help you improve your skills. Kaggle provides: Until now all our datasets have been available to download through fastai's integrated dataset system. However, the dataset we will be using in this chapter is only available from Kaggle. Therefore, you will need to register on the site, then go to the page for the competition. On that page click "Rules," then "I Understand and Accept." (Although the competition has finished, and you will not be entering it, you still have to agree to the rules to be allowed to download the data.) The easiest way to download Kaggle datasets is to use the Kaggle API. You can install this using You need an API key to use the Kaggle API; to get one, click on your profile picture on the Kaggle website, and choose My Account, then click Create New API Token. This will save a file called kaggle.json to your PC. You need to copy this key on your GPU server. To do so, open the file you downloaded, copy the contents, and paste them in the following cell in the notebook associated with this chapter (e.g., Then execute this cell (this only needs to be run once): Now you can download datasets from Kaggle! Pick a path to download the dataset to: And use the Kaggle API to download the dataset to that path, and extract it: Now that we have downloaded our dataset, let's take a look at it! Kaggle provides information about some of the fields of our dataset. The Data explains that the key fields in train.csv are: In any sort of data science work, it's important to look at your data directly to make sure you understand the format, how it's stored, what types of values it holds, etc. Even if you've read a description of the data, the actual data may not be what you expect. We'll start by reading the training set into a Pandas DataFrame. Generally it's a good idea to specify Let's load our data and have a look at the columns: That's a lot of columns for us to look at! Try looking through the dataset to get a sense of what kind of information is in each one. We'll shortly see how to "zero in" on the most interesting bits. At this point, a good next step is to handle ordinal columns. This refers to columns containing strings or similar, but where those strings have a natural ordering. For instance, here are the levels of We can tell Pandas about a suitable ordering of these levels like so: The most important data column is the dependent variable—that is, the one we want to predict. Recall that a model's metric is a function that reflects how good the predictions are. It's important to note what metric is being used for a project. Generally, selecting the metric is an important part of the project setup. In many cases, choosing a good metric will require more than just selecting a variable that already exists. It is more like a design process. You should think carefully about which metric, or set of metrics, actually measures the notion of model quality that matters to you. If no variable represents that metric, you should see if you can build the metric from the variables that are available. However, in this case Kaggle tells us what metric to use: root mean squared log error (RMSLE) between the actual and predicted auction prices. We need do only a small amount of processing to use this: we take the log of the prices, so that We are now ready to explore our first machine learning algorithm for tabular data: decision trees. Decision tree ensembles, as the name suggests, rely on decision trees. So let's start there! A decision tree asks a series of binary (that is, yes or no) questions about the data. After each question the data at that part of the tree is split between a "yes" and a "no" branch, as shown in < This sequence of questions is now a procedure for taking any data item, whether an item from the training set or a new one, and assigning that item to a group. Namely, after asking and answering the questions, we can say the item belongs to the same group as all the other training data items that yielded the same set of answers to the questions. But what good is this? The goal of our model is to predict values for items, not to assign them into groups from the training dataset. The value is that we can now assign a prediction value for each of these groups—for regression, we take the target mean of the items in the group. Let's consider how we find the right questions to ask. Of course, we wouldn't want to have to create all these questions ourselves—that's what computers are for! The basic steps to train a decision tree can be written down very easily: Although this is an easy enough algorithm to implement yourself (and it is a good exercise to do so), we can save some time by using the implementation built into sklearn. First, however, we need to do a little data preparation. A:Here's a productive question to ponder. If you consider that the procedure for defining a decision tree essentially chooses one sequence of splitting questions about variables, you might ask yourself, how do we know this procedure chooses the correct sequence? The rule is to choose the splitting question that produces the best split (i.e., that most accurately separates the items into two distinct categories), and then to apply the same rule to the groups that split produces, and so on. This is known in computer science as a "greedy" approach. Can you imagine a scenario in which asking a “less powerful” splitting question would enable a better split down the road (or should I say down the trunk!) and lead to a better result overall? The first piece of data preparation we need to do is to enrich our representation of dates. The fundamental basis of the decision tree that we just described is bisection— dividing a group into two. We look at the ordinal variables and divide up the dataset based on whether the variable's value is greater (or lower) than a threshold, and we look at the categorical variables and divide up the dataset based on whether the variable's level is a particular level. So this algorithm has a way of dividing up the dataset based on both ordinal and categorical data. But how does this apply to a common data type, the date? You might want to treat a date as an ordinal value, because it is meaningful to say that one date is greater than another. However, dates are a bit different from most ordinal values in that some dates are qualitatively different from others in a way that that is often relevant to the systems we are modeling. In order to help our algorithm handle dates intelligently, we'd like our model to know more than whether a date is more recent or less recent than another. We might want our model to make decisions based on that date's day of the week, on whether a day is a holiday, on what month it is in, and so forth. To do this, we replace every date column with a set of date metadata columns, such as holiday, day of week, and month. These columns provide categorical data that we suspect will be useful. fastai comes with a function that will do this for us—we just have to pass a column name that contains dates: Let's do the same for the test set while we're there: We can see that there are now lots of new columns in our DataFrame: This is a good first step, but we will need to do a bit more cleaning. For this, we will use fastai objects called A second piece of preparatory processing is to be sure we can handle strings and missing data. Out of the box, sklearn cannot do either. Instead we will use fastai's class Recall the distinction between a validation set and a test set, as discussed in < We don't get to see the test set. But we do want to define our validation data so that it has the same sort of relationship to the training data as the test set will have. In some cases, just randomly choosing a subset of your data points will do that. This is not one of those cases, because it is a time series. If you look at the date range represented in the test set, you will discover that it covers a six-month period from May 2012, which is later in time than any date in the training set. This is a good design, because the competition sponsor will want to ensure that a model is able to predict the future. But it means that if we are going to have a useful validation set, we also want the validation set to be later in time than the training set. The Kaggle training data ends in April 2012, so we will define a narrower training dataset which consists only of the Kaggle training data from before November 2011, and we'll define a validation set consisting of data from after November 2011. To do this we use A We can see that the data is still displayed as strings for categories (we only show a few columns here because the full table is too big to fit on a page): However, the underlying items are all numeric: The conversion of categorical columns to numbers is done by simply replacing each unique level with a number. The numbers associated with the levels are chosen consecutively as they are seen in a column, so there's no particular meaning to the numbers in categorical columns after conversion. The exception is if you first convert a column to a Pandas ordered category (as we did for Since it takes a minute or so to process the data to get to this point, we should save it—that way in the future we can continue our work from here without rerunning the previous steps. fastai provides a To read this back later, you would type: Now that all this preprocessing is done, we are ready to create a decision tree. To begin, we define our independent and dependent variables: Now that our data is all numeric, and there are no missing values, we can create a decision tree: To keep it simple, we've told sklearn to just create four leaf nodes. To see what it's learned, we can display the tree: Understanding this picture is one of the best ways to understand decision trees, so we will start at the top and explain each part step by step. The top node represents the initial model before any splits have been done, when all the data is in one group. This is the simplest possible model. It is the result of asking zero questions and will always predict the value to be the average value of the whole dataset. In this case, we can see it predicts a value of 10.10 for the logarithm of the sales price. It gives a mean squared error of 0.48. The square root of this is 0.69. (Remember that unless you see Moving down and to the left, this node shows us that there were 360,847 auction records for equipment where The bottom row contains our leaf nodes: the nodes with no answers coming out of them, because there are no more questions to be answered. At the far right of this row is the node containing records where Returning back to the top node after the first decision point, we can see that a second binary decision split has been made, based on asking whether We can show the same information using Terence Parr's powerful dtreeviz library: This shows a chart of the distribution of the data for each split point. We can clearly see that there's a problem with our That change makes the split much clearer in the tree visualization, even although it doesn't actually change the result of the model in any significant way. This is a great example of how resilient decision trees are to data issues! Let's now have the decision tree algorithm build a bigger tree. Here, we are not passing in any stopping criteria such as We'll create a little function to check the root mean squared error of our model ( So, our model is perfect, right? Not so fast... remember we really need to check the validation set, to ensure we're not overfitting: Oops—it looks like we might be overfitting pretty badly. Here's why: We've got nearly as many leaf nodes as data points! That seems a little over-enthusiastic. Indeed, sklearn's default settings allow it to continue splitting nodes until there is only one item in each leaf node. Let's change the stopping rule to tell sklearn to ensure every leaf node contains at least 25 auction records: That looks much better. Let's check the number of leaves again: Much more reasonable! A:Here's my intuition for an overfitting decision tree with more leaf nodes than data items. Consider the game Twenty Questions. In that game, the chooser secretly imagines an object (like, "our television set"), and the guesser gets to pose 20 yes or no questions to try to guess what the object is (like "Is it bigger than a breadbox?"). The guesser is not trying to predict a numerical value, but just to identify a particular object out of the set of all imaginable objects. When your decision tree has more leaves than there are possible objects in your domain, then it is essentially a well-trained guesser. It has learned the sequence of questions needed to identify a particular data item in the training set, and it is "predicting" only by describing that item's value. This is a way of memorizing the training set—i.e., of overfitting. Building a decision tree is a good way to create a model of our data. It is very flexible, since it can clearly handle nonlinear relationships and interactions between variables. But we can see there is a fundamental compromise between how well it generalizes (which we can achieve by creating small trees) and how accurate it is on the training set (which we can achieve by using large trees). So how do we get the best of both worlds? We'll show you right after we handle an important missing detail: how to handle categorical variables. In the previous chapter, when working with deep learning networks, we dealt with categorical variables by one-hot encoding them and feeding them to an embedding layer. The embedding layer helped the model to discover the meaning of the different levels of these variables (the levels of a categorical variable do not have an intrinsic meaning, unless we manually specify an ordering using Pandas). In a decision tree, we don't have embeddings layers—so how can these untreated categorical variables do anything useful in a decision tree? For instance, how could something like a product code be used? The short answer is: it just works! Think about a situation where there is one product code that is far more expensive at auction than any other one. In that case, any binary split will result in that one product code being in some group, and that group will be more expensive than the other group. Therefore, our simple decision tree building algorithm will choose that split. Later during training the algorithm will be able to further split the subgroup that contains the expensive product code, and over time, the tree will home in on that one expensive product. It is also possible to use one-hot encoding to replace a single categorical variable with multiple one-hot-encoded columns, where each column represents a possible level of the variable. Pandas has a However, there is not really any evidence that such an approach improves the end result. So, we generally avoid it where possible, because it does end up making your dataset harder to work with. In 2019 this issue was explored in the paper "Splitting on Categorical Predictors in Random Forests" by Marvin Wright and Inke König, which said: :The standard approach for nominal predictors is to consider all $2^{k-1} − 1$ 2-partitions of the k predictor categories. However, this exponential relationship produces a large number of potential splits to be evaluated, increasing computational complexity and restricting the possible number of categories in most implementations. For binary classification and regression, it was shown that ordering the predictor categories in each split leads to exactly the same splits as the standard approach. This reduces computational complexity because only k − 1 splits have to be considered for a nominal predictor with k categories. Now that you understand how decisions tree work, it's time for the best-of-both-worlds solution: random forests. In 1994 Berkeley professor Leo Breiman, one year after his retirement, published a small technical report called "Bagging Predictors", which turned out to be one of the most influential ideas in modern machine learning. The report began: :Bagging predictors is a method for generating multiple versions of a predictor and using these to get an aggregated predictor. The aggregation averages over the versions... The multiple versions are formed by making bootstrap replicates of the learning set and using these as new learning sets. Tests… show that bagging can give substantial gains in accuracy. The vital element is the instability of the prediction method. If perturbing the learning set can cause significant changes in the predictor constructed, then bagging can improve accuracy.

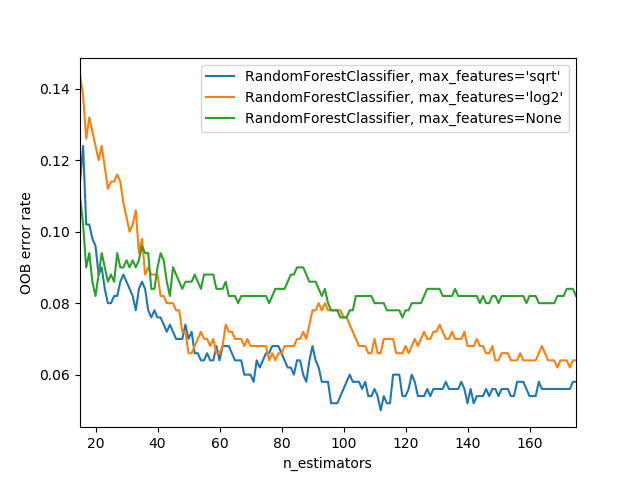

Here is the procedure that Breiman is proposing: This procedure is known as "bagging." It is based on a deep and important insight: although each of the models trained on a subset of data will make more errors than a model trained on the full dataset, those errors will not be correlated with each other. Different models will make different errors. The average of those errors, therefore, is: zero! So if we take the average of all of the models' predictions, then we should end up with a prediction that gets closer and closer to the correct answer, the more models we have. This is an extraordinary result—it means that we can improve the accuracy of nearly any kind of machine learning algorithm by training it multiple times, each time on a different random subset of the data, and averaging its predictions. In 2001 Leo Breiman went on to demonstrate that this approach to building models, when applied to decision tree building algorithms, was particularly powerful. He went even further than just randomly choosing rows for each model's training, but also randomly selected from a subset of columns when choosing each split in each decision tree. He called this method the random forest. Today it is, perhaps, the most widely used and practically important machine learning method. In essence a random forest is a model that averages the predictions of a large number of decision trees, which are generated by randomly varying various parameters that specify what data is used to train the tree and other tree parameters. Bagging is a particular approach to "ensembling," or combining the results of multiple models together. To see how it works in practice, let's get started on creating our own random forest! We can create a random forest just like we created a decision tree, except now, we are also specifying parameters that indicate how many trees should be in the forest, how we should subset the data items (the rows), and how we should subset the fields (the columns). In the following function definition Our validation RMSE is now much improved over our last result produced by the One of the most important properties of random forests is that they aren't very sensitive to the hyperparameter choices, such as The sklearn docs show an example of the effects of different To see the impact of As you can see, Let's see what happens to the RMSE as we add more and more trees. As you can see, the improvement levels off quite a bit after around 30 trees: The performance on our validation set is worse than on our training set. But is that because we're overfitting, or because the validation set covers a different time period, or a bit of both? With the existing information we've seen, we can't tell. However, random forests have a very clever trick called out-of-bag (OOB) error that can help us with this (and more!). Recall that in a random forest, each tree is trained on a different subset of the training data. The OOB error is a way of measuring prediction error on the training set by only including in the calculation of a row's error trees where that row was not included in training. This allows us to see whether the model is overfitting, without needing a separate validation set. A:My intuition for this is that, since every tree was trained with a different randomly selected subset of rows, out-of-bag error is a little like imagining that every tree therefore also has its own validation set. That validation set is simply the rows that were not selected for that tree's training.

This is particularly beneficial in cases where we have only a small amount of training data, as it allows us to see whether our model generalizes without removing items to create a validation set. The OOB predictions are available in the We can see that our OOB error is much lower than our validation set error. This means that something else is causing that error, in addition to normal generalization error. We'll discuss the reasons for this later in this chapter. This is one way to interpret our model's predictions—let's focus on more of those now. For tabular data, model interpretation is particularly important. For a given model, the things we are most likely to be interested in are: As we will see, random forests are particularly well suited to answering these questions. Let's start with the first one! We saw how the model averages the individual tree's predictions to get an overall prediction—that is, an estimate of the value. But how can we know the confidence of the estimate? One simple way is to use the standard deviation of predictions across the trees, instead of just the mean. This tells us the relative confidence of predictions. In general, we would want to be more cautious of using the results for rows where trees give very different results (higher standard deviations), compared to cases where they are more consistent (lower standard deviations). In the earlier section on creating a random forest, we saw how to get predictions over the validation set, using a Python list comprehension to do this for each tree in the forest: Now we have a prediction for every tree and every auction (40 trees and 7,988 auctions) in the validation set. Using this we can get the standard deviation of the predictions over all the trees, for each auction: Here are the standard deviations for the predictions for the first five auctions—that is, the first five rows of the validation set: As you can see, the confidence in the predictions varies widely. For some auctions, there is a low standard deviation because the trees agree. For others it's higher, as the trees don't agree. This is information that would be useful in a production setting; for instance, if you were using this model to decide what items to bid on at auction, a low-confidence prediction might cause you to look more carefully at an item before you made a bid. It's not normally enough just to know that a model can make accurate predictions—we also want to know how it's making predictions. feature importance gives us insight into this. We can get these directly from sklearn's random forest by looking in the The feature importances for our model show that the first few most important columns have much higher importance scores than the rest, with (not surprisingly) A plot of the feature importances shows the relative importances more clearly: The way these importances are calculated is quite simple yet elegant. The feature importance algorithm loops through each tree, and then recursively explores each branch. At each branch, it looks to see what feature was used for that split, and how much the model improves as a result of that split. The improvement (weighted by the number of rows in that group) is added to the importance score for that feature. This is summed across all branches of all trees, and finally the scores are normalized such that they add to 1. It seems likely that we could use just a subset of the columns by removing the variables of low importance and still get good results. Let's try just keeping those with a feature importance greater than 0.005: We can retrain our model using just this subset of the columns: And here's the result: Our accuracy is about the same, but we have far fewer columns to study: We've found that generally the first step to improving a model is simplifying it—78 columns was too many for us to study them all in depth! Furthermore, in practice often a simpler, more interpretable model is easier to roll out and maintain. This also makes our feature importance plot easier to interpret. Let's look at it again: One thing that makes this harder to interpret is that there seem to be some variables with very similar meanings: for example, Let's start with: In this chart, the pairs of columns that are most similar are the ones that were merged together early, far from the "root" of the tree at the left. Unsurprisingly, the fields Here's our baseline: Now we try removing each of our potentially redundant variables, one at a time: Now let's try dropping multiple variables. We'll drop one from each of the tightly aligned pairs we noticed earlier. Let's see what that does: Looking good! This is really not much worse than the model with all the fields. Let's create DataFrames without these columns, and save them: We can load them back later with: Now we can check our RMSE again, to confirm that the accuracy hasn't substantially changed. By focusing on the most important variables, and removing some redundant ones, we've greatly simplified our model. Now, let's see how those variables affect our predictions using partial dependence plots. As we've seen, the two most important predictors are The largrest group is Let's do the same thing for Other than the special value 1950 which we used for coding missing year values, most of the data is from after 1990. Now we're ready to look at partial dependence plots. Partial dependence plots try to answer the question: if a row varied on nothing other than the feature in question, how would it impact the dependent variable? For instance, how does To answer this question, we can't just take the average sale price for each Instead, what we do is replace every single value in the A:If you are philosophically minded it is somewhat dizzying to contemplate the different kinds of hypotheticality that we are juggling to make this calculation. First, there's the fact that every prediction is hypothetical, because we are not noting empirical data. Second, there's the point that we're not merely interested in asking how sale price would change if we changed Looking first of all at the The In the paper "Leakage in Data Mining: Formulation, Detection, and Avoidance", Shachar Kaufman, Saharon Rosset, and Claudia Perlich describe leakage as: :The introduction of information about the target of a data mining problem, which should not be legitimately available to mine from. A trivial example of leakage would be a model that uses the target itself as an input, thus concluding for example that 'it rains on rainy days'. In practice, the introduction of this illegitimate information is unintentional, and facilitated by the data collection, aggregation and preparation process.

They give as an example:

:A real-life business intelligence project at IBM where potential customers for certain products were identified, among other things, based on keywords found on their websites. This turned out to be leakage since the website content used for training had been sampled at the point in time where the potential customer has already become a customer, and where the website contained traces of the IBM products purchased, such as the word 'Websphere' (e.g., in a press release about the purchase or a specific product feature the client uses).

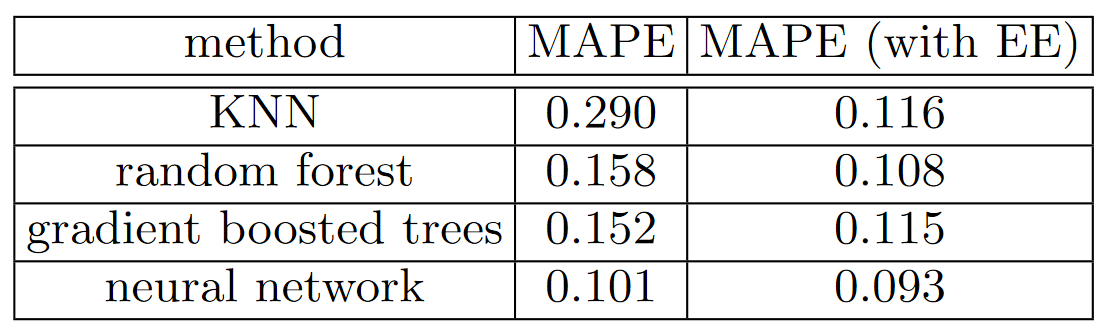

Data leakage is subtle and can take many forms. In particular, missing values often represent data leakage. For instance, Jeremy competed in a Kaggle competition designed to predict which researchers would end up receiving research grants. The information was provided by a university and included thousands of examples of research projects, along with information about the researchers involved and data on whether or not each grant was eventually accepted. The university hoped to be able to use the models developed in this competition to rank which grant applications were most likely to succeed, so it could prioritize its processing. Jeremy used a random forest to model the data, and then used feature importance to find out which features were most predictive. He noticed three surprising things: For the identifier columns, one partial dependence plot per column showed that when the information was missing the application was almost always rejected. It turned out that in practice, the university only filled out much of this information after a grant application was accepted. Often, for applications that were not accepted, it was just left blank. Therefore, this information was not something that was actually available at the time that the application was received, and it would not be available for a predictive model—it was data leakage. In the same way, the final processing of successful applications was often done automatically as a batch at the end of the week, or the end of the year. It was this final processing date which ended up in the data, so again, this information, while predictive, was not actually available at the time that the application was received. This example showcases the most practical and simple approaches to identifying data leakage, which are to build a model and then: Thinking back to our bear detector, this mirrors the advice that we provided in < It can also help you identify which factors influence specific predictions, with tree interpreters. At the start of this section, we said that we wanted to be able to answer five questions: We've handled four of these already; only the second question remains. To answer this question, we need to use the We have already seen how to compute feature importances across the entire random forest. The basic idea was to look at the contribution of each variable to improving the model, at each branch of every tree, and then add up all of these contributions per variable. We can do exactly the same thing, but for just a single row of data. For instance, let's say we are looking at some particular item at auction. Our model might predict that this item will be very expensive, and we want to know why. So, we take that one row of data and put it through the first decision tree, looking to see what split is used at each point throughout the tree. For each split, we see what the increase or decrease in the addition is, compared to the parent node of the tree. We do this for every tree, and add up the total change in importance by split variable. For instance, let's pick the first few rows of our validation set: We can then pass these to The clearest way to display the contributions is with a waterfall plot. This shows how the positive and negative contributions from all the independent variables sum up to create the final prediction, which is the righthand column labeled "net" here: This kind of information is most useful in production, rather than during model development. You can use it to provide useful information to users of your data product about the underlying reasoning behind the predictions. Now that we covered some classic machine learning techniques to solve this problem, let's see how deep learning can help! A problem with random forests, like all machine learning or deep learning algorithms, is that they don't always generalize well to new data. We will see in which situations neural networks generalize better, but first, let's look at the extrapolation problem that random forests have. Let's consider the simple task of making predictions from 40 data points showing a slightly noisy linear relationship: Although we only have a single independent variable, sklearn expects a matrix of independent variables, not a single vector. So we have to turn our vector into a matrix with one column. In other words, we have to change the shape from A more flexible approach is to slice an array or tensor with the special value We can now create a random forest for this data. We'll use only the first 30 rows to train the model: Then we'll test the model on the full dataset. The blue dots are the training data, and the red dots are the predictions: We have a big problem! Our predictions outside of the domain that our training data covered are all too low. Why do you suppose this is? Remember, a random forest just averages the predictions of a number of trees. And a tree simply predicts the average value of the rows in a leaf. Therefore, a tree and a random forest can never predict values outside of the range of the training data. This is particularly problematic for data where there is a trend over time, such as inflation, and you wish to make predictions for a future time. Your predictions will be systematically too low. But the problem extends beyond time variables. Random forests are not able to extrapolate outside of the types of data they have seen, in a more general sense. That's why we need to make sure our validation set does not contain out-of-domain data. Sometimes it is hard to know whether your test set is distributed in the same way as your training data, or, if it is different, what columns reflect that difference. There's actually an easy way to figure this out, which is to use a random forest! But in this case we don't use the random forest to predict our actual dependent variable. Instead, we try to predict whether a row is in the validation set or the training set. To see this in action, let's combine our training and validation sets together, create a dependent variable that represents which dataset each row comes from, build a random forest using that data, and get its feature importance: This shows that there are three columns that differ significantly between the training and validation sets: Let's get a baseline of the original random forest model's RMSE, then see what the effect is of removing each of these columns in turn: It looks like we should be able to remove Removing these variables has slightly improved the model's accuracy; but more importantly, it should make it more resilient over time, and easier to maintain and understand. We recommend that for all datasets you try building a model where your dependent variable is One thing that might help in our case is to simply avoid using old data. Often, old data shows relationships that just aren't valid any more. Let's try just using the most recent few years of the data: Here's the result of training on this subset: It's a tiny bit better, which shows that you shouldn't always just use your entire dataset; sometimes a subset can be better. Let's see if using a neural network helps. We can use the same approach to build a neural network model. Let's first replicate the steps we took to set up the We can leverage the work we did to trim unwanted columns in the random forest by using the same set of columns for our neural network: Categorical columns are handled very differently in neural networks, compared to decision tree approaches. As we saw in < In this case, there's one variable that we absolutely do not want to treat as categorical: the Let's take a look at the cardinality of each of the categorical variables that we have chosen so far: The fact that there are two variables pertaining to the "model" of the equipment, both with similar very high cardinalities, suggests that they may contain similar, redundant information. Note that we would not necessarily see this when analyzing redundant features, since that relies on similar variables being sorted in the same order (that is, they need to have similarly named levels). Having a column with 5,000 levels means needing 5,000 columns in our embedding matrix, which would be nice to avoid if possible. Let's see what the impact of removing one of these model columns has on the random forest: There's minimal impact, so we will remove it as a predictor for our neural network: We can create our Tabular models and data don't generally require much GPU RAM, so we can use larger batch sizes: As we've discussed, it's a good idea to set We can now create the By default, for tabular data fastai creates a neural network with two hidden layers, with 200 and 100 activations, respectively. This works quite well for small datasets, but here we've got quite a large dataset, so we increase the layer sizes to 500 and 250: There's no need to use We can use our It's quite a bit better than the random forest (although it took longer to train, and it's fussier about hyperparameter tuning). Before we move on, let's save our model in case we want to come back to it again later: In fastai, a tabular model is simply a model that takes columns of continuous or categorical data, and predicts a category (a classification model) or a continuous value (a regression model). Categorical independent variables are passed through an embedding, and concatenated, as we saw in the neural net we used for collaborative filtering, and then continuous variables are concatenated as well. The model created in That means that really all the work is happening in Another thing that can help with generalization is to use several models and average their predictions—a technique, as mentioned earlier, known as ensembling. Think back to the original reasoning behind why random forests work so well: each tree has errors, but those errors are not correlated with each other, so the average of those errors should tend towards zero once there are enough trees. Similar reasoning could be used to consider averaging the predictions of models trained using different algorithms. In our case, we have two very different models, trained using very different algorithms: a random forest, and a neural network. It would be reasonable to expect that the kinds of errors that each one makes would be quite different. Therefore, we might expect that the average of their predictions would be better than either one's individual predictions. As we saw earlier, a random forest is itself an ensemble. But we can then include a random forest in another ensemble—an ensemble of the random forest and the neural network! While ensembling won't make the difference between a successful and an unsuccessful modeling process, it can certainly add a nice little boost to any models that you have built. One minor issue we have to be aware of is that our PyTorch model and our sklearn model create data of different types: PyTorch gives us a rank-2 tensor (i.e, a column matrix), whereas NumPy gives us a rank-1 array (a vector). This gives us a better result than either model achieved on its own: In fact, this result is better than any score shown on the Kaggle leaderboard. It's not directly comparable, however, because the Kaggle leaderboard uses a separate dataset that we do not have access to. Kaggle does not allow us to submit to this old competition to find out how we would have done, but our results certainly look very encouraging! So far our approach to ensembling has been to use bagging, which involves combining many models (each trained on a different data subset) together by averaging them. As we saw, when this is applied to decision trees, this is called a random forest. There is another important approach to ensembling, called boosting, where we add models instead of averaging them. Here is how boosting works: Using this approach, each new tree will be attempting to fit the error of all of the previous trees combined. Because we are continually creating new residuals, by subtracting the predictions of each new tree from the residuals from the previous tree, the residuals will get smaller and smaller. To make predictions with an ensemble of boosted trees, we calculate the predictions from each tree, and then add them all together. There are many models following this basic approach, and many names for the same models. Gradient boosting machines (GBMs) and gradient boosted decision trees (GBDTs) are the terms you're most likely to come across, or you may see the names of specific libraries implementing these; at the time of writing, XGBoost is the most popular. Note that, unlike with random forests, with this approach there is nothing to stop us from overfitting. Using more trees in a random forest does not lead to overfitting, because each tree is independent of the others. But in a boosted ensemble, the more trees you have, the better the training error becomes, and eventually you will see overfitting on the validation set. We are not going to go into detail on how to train a gradient boosted tree ensemble here, because the field is moving rapidly, and any guidance we give will almost certainly be outdated by the time you read this. As we write this, sklearn has just added a One more technique that has gotten great results is to use embeddings learned by a neural net in a machine learning model. The abstract of the entity embedding paper we mentioned at the start of this chapter states: "the embeddings obtained from the trained neural network boost the performance of all tested machine learning methods considerably when used as the input features instead". It includes the very interesting table in < This is showing the mean average percent error (MAPE) compared among four different modeling techniques, three of which we have already seen, along with k-nearest neighbors (KNN), which is a very simple baseline method. The first numeric column contains the results of using the methods on the data provided in the competition; the second column shows what happens if you first train a neural network with categorical embeddings, and then use those categorical embeddings instead of the raw categorical columns in the model. As you see, in every case, the models are dramatically improved by using the embeddings instead of the raw categories. This is a really important result, because it shows that you can get much of the performance improvement of a neural network without actually having to use a neural network at inference time. You could just use an embedding, which is literally just an array lookup, along with a small decision tree ensemble. These embeddings need not even be necessarily learned separately for each model or task in an organization. Instead, once a set of embeddings are learned for some column for some task, they could be stored in a central place, and reused across multiple models. In fact, we know from private communication with other practitioners at large companies that this is already happening in many places. We have dicussed two approaches to tabular modeling: decision tree ensembles and neural networks. We've also mentioned two different decision tree ensembles: random forests, and gradient boosting machines. Each is very effective, but each also has compromises: Random forests are the easiest to train, because they are extremely resilient to hyperparameter choices and require very little preprocessing. They are very fast to train, and should not overfit if you have enough trees. But they can be a little less accurate, especially if extrapolation is required, such as predicting future time periods. Gradient boosting machines in theory are just as fast to train as random forests, but in practice you will have to try lots of different hyperparameters. They can overfit, but they are often a little more accurate than random forests. Neural networks take the longest time to train, and require extra preprocessing, such as normalization; this normalization needs to be used at inference time as well. They can provide great results and extrapolate well, but only if you are careful with your hyperparameters and take care to avoid overfitting. We suggest starting your analysis with a random forest. This will give you a strong baseline, and you can be confident that it's a reasonable starting point. You can then use that model for feature selection and partial dependence analysis, to get a better understanding of your data. From that foundation, you can try neural nets and GBMs, and if they give you significantly better results on your validation set in a reasonable amount of time, you can use them. If decision tree ensembles are working well for you, try adding the embeddings for the categorical variables to the data, and see if that helps your decision trees learn better.

State category. For a categorical variable we call the possible values of the variable its "levels" (or "categories" or "classes"), so here one level is "Berlin," another is "Hamburg," etc. On the right is a map of Germany. The actual physical locations of the German states were not part of the provided data, yet the model itself learned where they must be, based only on the behavior of store sales!

sklearn). Scikit-learn is a popular library for creating machine learning models, using approaches that are not covered by deep learning. In addition, we'll need to do some tabular data processing and querying, so we'll want to use the Pandas library. Finally, we'll also need NumPy, since that's the main numeric programming library that both sklearn and Pandas rely on.

pip by running this in a notebook cell:!pip install kaggle

creds = '{"username":"xxx","key":"xxx"}'):creds = '{"username":"nikemr","key":"33d71d96879caa193ff2e354a50bed97"}'

cred_path = Path('~/.kaggle/kaggle.json').expanduser()

if not cred_path.exists():

cred_path.parent.mkdir(exist_ok=True)

cred_path.write_text(creds)

cred_path.chmod(0o600)

path = URLs.path('bluebook')

path

path.ls()

if not path.exists():

path.mkdir(parents=true)

api.competition_download_cli('bluebook-for-bulldozers', path=path)

file_extract(path/'bluebook-for-bulldozers.zip')

path.ls(file_type='text')

file_extract(path/'bluebook-for-bulldozers.zip')

unzip bluebook-for-bulldozers.zip

SalesID:: The unique identifier of the sale.MachineID:: The unique identifier of a machine. A machine can be sold multiple times.saleprice:: What the machine sold for at auction (only provided in train.csv).saledate:: The date of the sale.low_memory=False unless Pandas actually runs out of memory and returns an error. The low_memory parameter, which is True by default, tells Pandas to only look at a few rows of data at a time to figure out what type of data is in each column. This means that Pandas can actually end up using different data type for different rows, which generally leads to data processing errors or model training problems later.low_memory=False

df = pd.read_csv(path/'TrainAndValid.csv', low_memory=False)

df.columns

ProductSize:df['ProductSize'].unique()

sizes = 'Large','Large / Medium','Medium','Small','Mini','Compact'

df['ProductSize'] = df['ProductSize'].astype('category')

df['ProductSize'].cat.set_categories(sizes, ordered=True, inplace=True)

df['ProductSize'].unique()

rmse of that value will give us what we ultimately need:dep_var = 'SalePrice'

df[dep_var] = np.log(df[dep_var])

df = add_datepart(df, 'saledate')

df_test = pd.read_csv(path/'Test.csv', low_memory=False)

df_test = add_datepart(df_test, 'saledate')

' '.join(o for o in df.columns if o.startswith('sale'))

TabularPandas and TabularProc.TabularPandas, which wraps a Pandas DataFrame and provides a few conveniences. To populate a TabularPandas, we will use two TabularProcs, Categorify and FillMissing. A TabularProc is like a regular Transform, except that:

Categorify is a TabularProc that replaces a column with a numeric categorical column. FillMissing is a TabularProc that replaces missing values with the median of the column, and creates a new Boolean column that is set to True for any row where the value was missing. These two transforms are needed for nearly every tabular dataset you will use, so this is a good starting point for your data processing:procs = [Categorify, FillMissing]

TabularPandas will also handle splitting the dataset into training and validation sets for us. However we need to be very careful about our validation set. We want to design it so that it is like the test set Kaggle will use to judge the contest.np.where, a useful function that returns (as the first element of a tuple) the indices of all True values:cond = (df.saleYear<2011) | (df.saleMonth<10)

train_idx = np.where( cond)[0]

valid_idx = np.where(~cond)[0]

splits = (list(train_idx),list(valid_idx))

TabularPandas needs to be told which columns are continuous and which are categorical. We can handle that automatically using the helper function cont_cat_split:cont,cat = cont_cat_split(df, 1, dep_var=dep_var)

to = TabularPandas(df, procs, cat, cont, y_names=dep_var, splits=splits)

TabularPandas behaves a lot like a fastai Datasets object, including providing train and valid attributes:len(to.train),len(to.valid)

to.show(3)

to.items.head(3)

ProductSize earlier), in which case the ordering you chose is used. We can see the mapping by looking at the classes attribute:to.classes['ProductSize']

save method that uses Python's pickle system to save nearly any Python object:save_pickle(path/'to.pkl',to)

to = (path/'to.pkl').load()

xs,y = to.train.xs,to.train.y

valid_xs,valid_y = to.valid.xs,to.valid.y

m = DecisionTreeRegressor(max_leaf_nodes=4)

m.fit(xs, y);

draw_tree(m, xs, size=10, leaves_parallel=True, precision=2)

m_rmse, or a root mean squared error, then the value you are looking at is before taking the square root, so it is just the average of the square of the differences.) We can also see that there are 404,710 auction records in this group—that is the total size of our training set. The final piece of information shown here is the decision criterion for the best split that was found, which is to split based on the coupler_system column.coupler_system was less than 0.5. The average value of our dependent variable in this group is 10.21. Moving down and to the right from the initial model takes us to the records where coupler_system was greater than 0.5.coupler_system was greater than 0.5. The average value here is 9.21, so we can see the decision tree algorithm did find a single binary decision that separated high-value from low-value auction results. Asking only about coupler_system predicts an average value of 9.21 versus 10.1.YearMade is less than or equal to 1991.5. For the group where this is true (remember, this is now following two binary decisions, based on coupler_system and YearMade) the average value is 9.97, and there are 155,724 auction records in this group. For the group of auctions where this decision is false, the average value is 10.4, and there are 205,123 records. So again, we can see that the decision tree algorithm has successfully split our more expensive auction records into two more groups which differ in value significantly.samp_idx = np.random.permutation(len(y))[:500]

dtreeviz(m, xs.iloc[samp_idx], y.iloc[samp_idx], xs.columns, dep_var,

fontname='DejaVu Sans', scale=1.6, label_fontsize=10,

orientation='LR')

YearMade data: there are bulldozers made in the year 1000, apparently! Presumably this is actually just a missing value code (a value that doesn't otherwise appear in the data and that is used as a placeholder in cases where a value is missing). For modeling purposes, 1000 is fine, but as you can see this outlier makes visualization of the values we are interested in more difficult. So, let's replace it with 1950:xs.loc[xs['YearMade']<1900, 'YearMade'] = 1950

valid_xs.loc[valid_xs['YearMade']<1900, 'YearMade'] = 1950

m = DecisionTreeRegressor(max_leaf_nodes=4).fit(xs, y)

dtreeviz(m, xs.iloc[samp_idx], y.iloc[samp_idx], xs.columns, dep_var,

fontname='DejaVu Sans', scale=1.6, label_fontsize=10,

orientation='LR')

max_leaf_nodes:m = DecisionTreeRegressor()

m.fit(xs, y);

m_rmse), since that's how the competition was judged:def r_mse(pred,y): return round(math.sqrt(((pred-y)**2).mean()), 6)

def m_rmse(m, xs, y): return r_mse(m.predict(xs), y)

m_rmse(m, xs, y)

m_rmse(m, valid_xs, valid_y)

m.get_n_leaves(), len(xs)

m = DecisionTreeRegressor(min_samples_leaf=25)

m.fit(to.train.xs, to.train.y)

m_rmse(m, xs, y), m_rmse(m, valid_xs, valid_y)

m.get_n_leaves()

get_dummies method which does just that.

n_estimators defines the number of trees we want, max_samples defines how many rows to sample for training each tree, and max_features defines how many columns to sample at each split point (where 0.5 means "take half the total number of columns"). We can also specify when to stop splitting the tree nodes, effectively limiting the depth of the tree, by including the same min_samples_leaf parameter we used in the last section. Finally, we pass n_jobs=-1 to tell sklearn to use all our CPUs to build the trees in parallel. By creating a little function for this, we can more quickly try different variations in the rest of this chapter:def rf(xs, y, n_estimators=40, max_samples=200_000,

max_features=0.5, min_samples_leaf=5, **kwargs):

return RandomForestRegressor(n_jobs=-1, n_estimators=n_estimators,

max_samples=max_samples, max_features=max_features,

min_samples_leaf=min_samples_leaf, oob_score=True).fit(xs, y)

m = rf(xs, y);

DecisionTreeRegressor, which made just one tree using all the available data:m_rmse(m, xs, y), m_rmse(m, valid_xs, valid_y)

max_features. You can set n_estimators to as high a number as you have time to train—the more trees you have, the more accurate the model will be. max_samples can often be left at its default, unless you have over 200,000 data points, in which case setting it to 200,000 will make it train faster with little impact on accuracy. max_features=0.5 and min_samples_leaf=4 both tend to work well, although sklearn's defaults work well too.max_features choices, with increasing numbers of trees. In the plot, the blue plot line uses the fewest features and the green line uses the most (it uses all the features). As you can see in <

n_estimators, let's get the predictions from each individual tree in our forest (these are in the estimators_ attribute):preds = np.stack([t.predict(valid_xs) for t in m.estimators_])

preds.mean(0) gives the same results as our random forest:r_mse(preds.mean(0), valid_y)

plt.plot([r_mse(preds[:i+1].mean(0), valid_y) for i in range(40)]);

oob_prediction_ attribute. Note that we compare them to the training labels, since this is being calculated on trees using the training set.r_mse(m.oob_prediction_, y)

preds = np.stack([t.predict(valid_xs) for t in m.estimators_])

preds.shape

preds_std = preds.std(0)

preds_std[:5]

feature_importances_ attribute. Here's a simple function we can use to pop them into a DataFrame and sort them:def rf_feat_importance(m, df):

return pd.DataFrame({'cols':df.columns, 'imp':m.feature_importances_}

).sort_values('imp', ascending=False)

YearMade and ProductSize being at the top of the list:fi = rf_feat_importance(m, xs)

fi[:10]

def plot_fi(fi):

return fi.plot('cols', 'imp', 'barh', figsize=(12,7), legend=False)

plot_fi(fi[:30]);

to_keep = fi[fi.imp>0.005].cols

len(to_keep)

xs_imp = xs[to_keep]

valid_xs_imp = valid_xs[to_keep]

m = rf(xs_imp, y)

m_rmse(m, xs_imp, y), m_rmse(m, valid_xs_imp, valid_y)

len(xs.columns), len(xs_imp.columns)

plot_fi(rf_feat_importance(m, xs_imp));

ProductGroup and ProductGroupDesc. Let's try to remove any redundent features.cluster_columns(xs_imp)

ProductGroup and ProductGroupDesc were merged quite early, as were saleYear and saleElapsed and fiModelDesc and fiBaseModel. These might be so closely correlated they are practically synonyms for each other.

max_samples and higher min_samples_leaf. The OOB score is a number returned by sklearn that ranges between 1.0 for a perfect model and 0.0 for a random model. (In statistics it's called R^2, although the details aren't important for this explanation.) We don't need it to be very accurate—we're just going to use it to compare different models, based on removing some of the possibly redundant columns:

def get_oob(df):

m = RandomForestRegressor(n_estimators=40, min_samples_leaf=15,

max_samples=50000, max_features=0.5, n_jobs=-1, oob_score=True)

m.fit(df, y)

return m.oob_score_

get_oob(xs_imp)

{c:get_oob(xs_imp.drop(c, axis=1)) for c in (

'saleYear', 'saleElapsed', 'ProductGroupDesc','ProductGroup',

'fiModelDesc', 'fiBaseModel',

'Hydraulics_Flow','Grouser_Tracks', 'Coupler_System')}

to_drop = ['saleYear', 'ProductGroupDesc', 'fiBaseModel', 'Grouser_Tracks']

get_oob(xs_imp.drop(to_drop, axis=1))

xs_final = xs_imp.drop(to_drop, axis=1)

valid_xs_final = valid_xs_imp.drop(to_drop, axis=1)

save_pickle(path/'xs_final.pkl', xs_final)

save_pickle(path/'valid_xs_final.pkl', valid_xs_final)

xs_final = load_pickle(path/'xs_final.pkl')

valid_xs_final = load_pickle(path/'valid_xs_final.pkl')

m = rf(xs_final, y)

m_rmse(m, xs_final, y), m_rmse(m, valid_xs_final, valid_y)

ProductSize and YearMade. We'd like to understand the relationship between these predictors and sale price. It's a good idea to first check the count of values per category (provided by the Pandas value_counts method), to see how common each category is:p = valid_xs_final['ProductSize'].value_counts(sort=False).plot.barh()

c = to.classes['ProductSize']

plt.yticks(range(len(c)), c);

#na#, which is the label fastai applies to missing values.YearMade. Since this is a numeric feature, we'll need to draw a histogram, which groups the year values into a few discrete bins:ax = valid_xs_final['YearMade'].hist()

YearMade impact sale price, all other things being equal?YearMade. The problem with that approach is that many other things vary from year to year as well, such as which products are sold, how many products have air-conditioning, inflation, and so forth. So, merely averaging over all the auctions that have the same YearMade would also capture the effect of how every other field also changed along with YearMade and how that overall change affected price.YearMade column with 1950, and then calculate the predicted sale price for every auction, and take the average over all auctions. Then we do the same for 1951, 1952, and so forth until our final year of 2011. This isolates the effect of only YearMade (even if it does so by averaging over some imagined records where we assign a YearMade value that might never actually exist alongside some other values).

YearMade and everything else along with it. Rather, we're very specifically asking, how sale price would change in a hypothetical world where only YearMade changed. Phew! It is impressive that we can ask such questions. I recommend Judea Pearl and Dana Mackenzie's recent book on causality, The Book of Why (Basic Books), if you're interested in more deeply exploring formalisms for analyzing these subtleties.

With these averages, we can then plot each of these years on the x-axis, and each of the predictions on the y-axis. This, finally, is a partial dependence plot. Let's take a look:from sklearn.inspection import plot_partial_dependence

fig,ax = plt.subplots(figsize=(12, 4))

plot_partial_dependence(m, valid_xs_final, ['YearMade','ProductSize'],

grid_resolution=20, ax=ax);

YearMade plot, and specifically at the section covering the years after 1990 (since as we noted this is where we have the most data), we can see a nearly linear relationship between year and price. Remember that our dependent variable is after taking the logarithm, so this means that in practice there is an exponential increase in price. This is what we would expect: depreciation is generally recognized as being a multiplicative factor over time, so, for a given sale date, varying year made ought to show an exponential relationship with sale price.ProductSize partial plot is a bit concerning. It shows that the final group, which we saw is for missing values, has the lowest price. To use this insight in practice, we would want to find out why it's missing so often, and what that means. Missing values can sometimes be useful predictors—it entirely depends on what causes them to be missing. Sometimes, however, they can indicate data leakage.

treeinterpreter library. We'll also use the waterfallcharts library to draw the chart of the results.!pip install treeinterpreter

!pip install waterfallchartsrow = valid_xs_final.iloc[:5]

treeinterpreter:prediction,bias,contributions = treeinterpreter.predict(m, row.values)

prediction is simply the prediction that the random forest makes. bias is the prediction based on taking the mean of the dependent variable (i.e., the model that is the root of every tree). contributions is the most interesting bit—it tells us the total change in predicition due to each of the independent variables. Therefore, the sum of contributions plus bias must equal the prediction, for each row. Let's look just at the first row:prediction[0], bias[0], contributions[0].sum()

waterfall(valid_xs_final.columns, contributions[0], threshold=0.08,

rotation_value=45,formatting='{:,.3f}');

x_lin = torch.linspace(0,20, steps=40)

y_lin = x_lin + torch.randn_like(x_lin)

plt.scatter(x_lin, y_lin);

[40] to [40,1]. One way to do that is with the unsqueeze method, which adds a new unit axis to a tensor at the requested dimension:xs_lin = x_lin.unsqueeze(1)

x_lin.shape,xs_lin.shape

None, which introduces an additional unit axis at that location:x_lin[:,None].shape

m_lin = RandomForestRegressor().fit(xs_lin[:30],y_lin[:30])

plt.scatter(x_lin, y_lin, 20)

plt.scatter(x_lin, m_lin.predict(xs_lin), color='red', alpha=0.5);

df_dom = pd.concat([xs_final, valid_xs_final])

is_valid = np.array([0]*len(xs_final) + [1]*len(valid_xs_final))

m = rf(df_dom, is_valid)

rf_feat_importance(m, df_dom)[:6]

saleElapsed, SalesID, and MachineID. It's fairly obvious why this is the case for saleElapsed: it's the number of days between the start of the dataset and each row, so it directly encodes the date. The difference in SalesID suggests that identifiers for auction sales might increment over time. MachineID suggests something similar might be happening for individual items sold in those auctions.m = rf(xs_final, y)

print('orig', m_rmse(m, valid_xs_final, valid_y))

for c in ('SalesID','saleElapsed','MachineID'):

m = rf(xs_final.drop(c,axis=1), y)

print(c, m_rmse(m, valid_xs_final.drop(c,axis=1), valid_y))

SalesID and MachineID without losing any accuracy. Let's check:time_vars = ['SalesID','MachineID']

xs_final_time = xs_final.drop(time_vars, axis=1)

valid_xs_time = valid_xs_final.drop(time_vars, axis=1)

m = rf(xs_final_time, y)

m_rmse(m, valid_xs_time, valid_y)

is_valid, like we did here. It can often uncover subtle domain shift issues that you may otherwise miss.xs['saleYear'].hist();

filt = xs['saleYear']>2004

xs_filt = xs_final_time[filt]

y_filt = y[filt]

m = rf(xs_filt, y_filt)

m_rmse(m, xs_filt, y_filt), m_rmse(m, valid_xs_time, valid_y)

TabularPandas object:df_nn = pd.read_csv(path/'TrainAndValid.csv', low_memory=False)

df_nn['ProductSize'] = df_nn['ProductSize'].astype('category')

df_nn['ProductSize'].cat.set_categories(sizes, ordered=True, inplace=True)

df_nn[dep_var] = np.log(df_nn[dep_var])

df_nn = add_datepart(df_nn, 'saledate')

df_nn_final = df_nn[list(xs_final_time.columns) + [dep_var]]

max_card parameter. If it's lower, fastai will treat the variable as categorical. Embedding sizes larger than 10,000 should generally only be used after you've tested whether there are better ways to group the variable, so we'll use 9,000 as our max_card:</p>

</div>

</div>

</div>

cont_nn,cat_nn = cont_cat_split(df_nn_final, max_card=9000, dep_var=dep_var)

saleElapsed variable. A categorical variable cannot, by definition, extrapolate outside the range of values that it has seen, but we want to be able to predict auction sale prices in the future. Let's verify that cont_cat_split did the correct thing.cont_nn

df_nn_final[cat_nn].nunique()

xs_filt2 = xs_filt.drop('fiModelDescriptor', axis=1)

valid_xs_time2 = valid_xs_time.drop('fiModelDescriptor', axis=1)

m2 = rf(xs_filt2, y_filt)

m_rmse(m2, xs_filt2, y_filt), m_rmse(m2, valid_xs_time2, valid_y)

cat_nn.remove('fiModelDescriptor')

TabularPandas object in the same way as when we created our random forest, with one very important addition: normalization. A random forest does not need any normalization—the tree building procedure cares only about the order of values in a variable, not at all about how they are scaled. But as we have seen, a neural network definitely does care about this. Therefore, we add the Normalize processor when we build our TabularPandas object:procs_nn = [Categorify, FillMissing, Normalize]

to_nn = TabularPandas(df_nn_final, procs_nn, cat_nn, cont_nn,

splits=splits, y_names=dep_var)

dls = to_nn.dataloaders(1024)

y_range for regression models, so let's find the min and max of our dependent variable:y = to_nn.train.y

y.min(),y.max()

Learner to create this tabular model. As usual, we use the application-specific learner function, to take advantage of its application-customized defaults. We set the loss function to MSE, since that's what this competition uses.learn = tabular_learner(dls, y_range=(8,12), layers=[500,250],

n_out=1, loss_func=F.mse_loss)

learn.lr_find()

fine_tune, so we'll train with fit_one_cycle for a few epochs and see how it looks:learn.fit_one_cycle(5, 0.000158)

r_mse function to compare the result to the random forest result we got earlier:preds,targs = learn.get_preds()

r_mse(preds,targs)

learn.save('nn')

tabular_learner is an object of class TabularModel. Take a look at the source for tabular_learner now (remember, that's tabular_learner?? in Jupyter). You'll see that like collab_learner, it first calls get_emb_sz to calculate appropriate embedding sizes (you can override these by using the emb_szs parameter, which is a dictionary containing any column names you want to set sizes for manually), and it sets a few other defaults. Other than that, it just creates the TabularModel, and passes that to TabularLearner (note that TabularLearner is identical to Learner, except for a customized predict method).TabularModel, so take a look at the source for that now. With the exception of the BatchNorm1d and Dropout layers (which we'll be learning about shortly), you now have the knowledge required to understand this whole class. Take a look at the discussion of EmbeddingNN at the end of the last chapter. Recall that it passed n_cont=0 to TabularModel. We now can see why that was: because there are zero continuous variables (in fastai the n_ prefix means "number of," and cont is an abbreviation for "continuous").squeeze removes any unit axes from a tensor, and to_np converts it into a NumPy array:rf_preds = m.predict(valid_xs_time)

ens_preds = (to_np(preds.squeeze()) + rf_preds) /2

r_mse(ens_preds,valid_y)

HistGradientBoostingRegressor class that provides excellent performance. There are many hyperparameters to tweak for this class, and for all gradient boosted tree methods we have seen. Unlike random forests, gradient boosted trees are extremely sensitive to the choices of these hyperparameters; in practice, most people use a loop that tries a range of different hyperparameters to find the ones that work best.

mse, samples, and values calculated in the decision tree drawn in this chapter?max_samples and max_features when creating a random forest?n_estimators to a very high value, can that lead to overfitting? Why or why not?preds.mean(0) give the same result as our random forest?</li>

saleElapsed is a continuous variable, even although it has less than 9,000 distinct values?

TabularModel does (with the exception of the BatchNorm1d and Dropout layers).